Home renovation projects can easily snowball, and there are multiple ways out there to finance the undertaking. To help you assess the financial viability of your remodeling project, below we discuss why you might find borrowing for a renovation project helpful, as well as some precautions before you knock on the bank’s door.

Renovation loans can boost your returns

Aside from enabling people to get one step closer to their dream homes, renovation loans can also help investor-minded homeowners to boost the returns on their home remodeling projects. This is especially true if the property was bought at a depressed value for some reason (old, flooded, burnt, etc.), and needs a face-lift to prepare for a fix-and-flip.

Suppose you bought a depressed 3-room flat for S$240,000 in Jurong East. If you have S$5,000 at hand and use only this budget to renovate your property, you will probably run out of money even before you notice any difference. Effectively, you are unlikely to recoup any meaningful returns because your property probably looks the same, and it can only sell for about the same price that you purchased it for. Considering the time and effort you put towards the renovation and the transaction costs, this sounds like a bad deal.

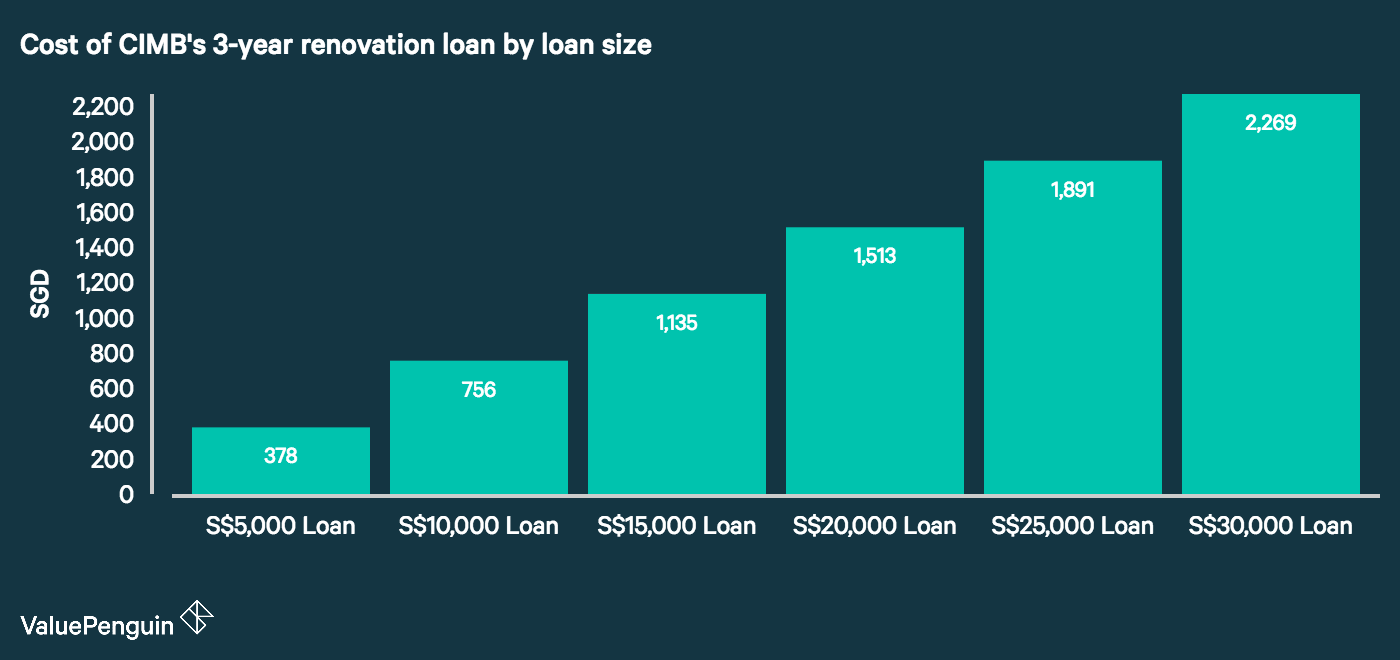

However, if you borrow an additional S$25,000 of renovation loan, you can enlarge your home improvement project. Although you will incur about S$1,891 in additional interest (assuming CIMB’s 3-year renovation loan), what you get in return, will almost certainly justify this cost. This is because you’ll have sufficient budget to make your house functional and inhabitable. Based on the property price in Jurong East, your now-functional 3-room property could sell at around S$300,000, which can result in a net profit of S$28,109.

Watch out for interest costs that eat out your returns

However, borrowing to do a larger-scale project isn’t always the best idea, especially if your property is already functional and the nature of the renovation is for luxury. This is because renovation tends to have a diminishing marginal return as the project gets more expensive. For example, let’s say you can do either a S$30,000 or a S$50,000 kitchen renovation project. If you are financing the project with 100% loan, then the total interest costs you will incur are S$2,269 and S$3,782, respectively, with a difference of S$1,513 in incremental interest cost.

However, you should carefully investigate whether a S$50,000 kitchen can recoup more profit than a S$30,000 one to justify the S$1,500 cost. This is because high-end features and functionalities become more personalised, and a potential buyer may not value certain things like expensive materials and built-in dishwashers in the first place. Your buyer will pay you more than your cost if and only if the renovation work is at least as good as (if not better than) what they would’ve done on their own anyway. For getting a relatively large loan, therefore, you should be careful about how the increased cost of debt might affect your net position given that luxury projects tend to yield less returns.

Personal loans are double-edged swords

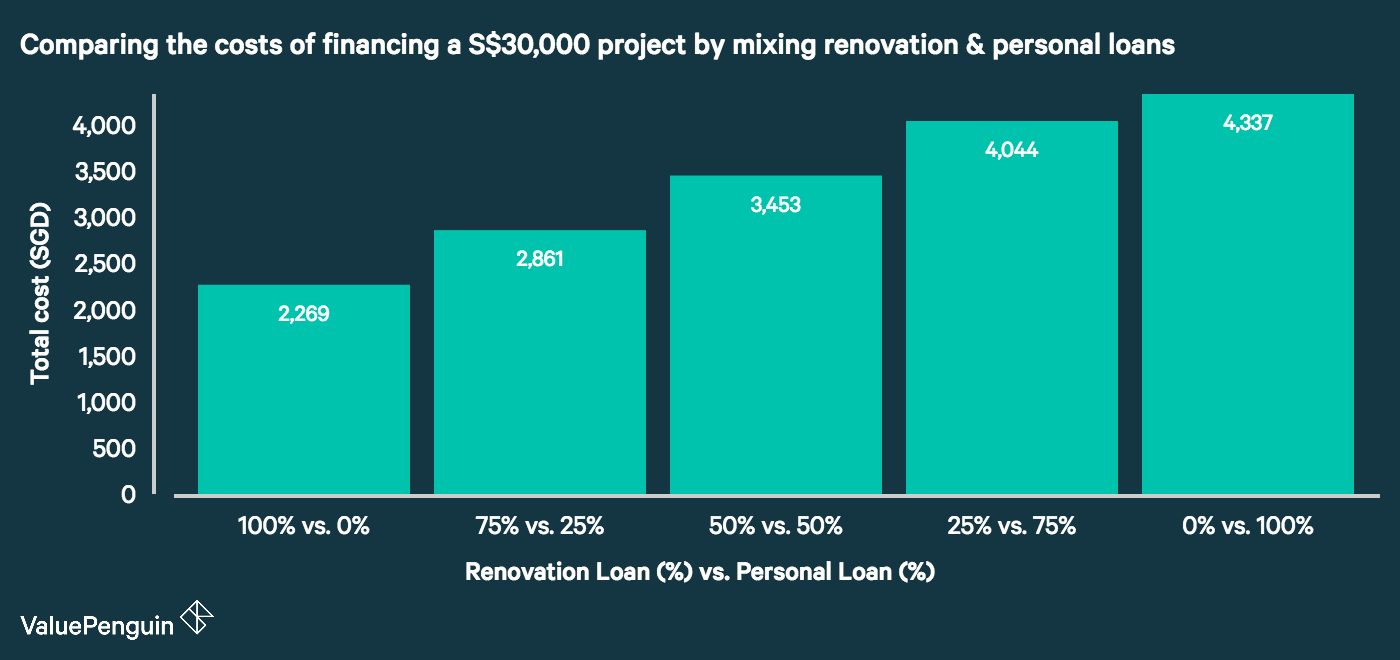

As a rule of thumb, you should always get a renovation loan instead of a personal loan if you can due to their 5-7% cheaper interest rates. However, you might need additional funding from a personal loan to do a large project if you need more than the limit on how much you can borrow from a renovation loan (S$30,000 or 6-10x your monthly income). In such cases, however, you should be especially careful about the higher interest cost you have to pay.

For instance, let’s take a look at two ways of financing (borrowing with 100% renovation loan vs. borrowing with 50% renovation loan & 50% personal loan) for a S$30,000 project that can increase your home’s resale value by S$33,000. If you take out a 3-year S$30,000 renovation loan from CIMB to finance the project, you will incur a total cost of S$2,269, which decreases your S$3,000 profit to S$731 (but you will still break-even). However, if you take out a S$15,000 renovation loan from CIMB and finance the rest using HSBC’s personal loan, you will incur a total interest cost of S$3,303. Owing to the personal loan’s high interest of 9%, your project is no longer profitable.

In general, personal loans are not the best ways to finance a home renovation project, especially if renovation loans are available to you. You should only take on the risk of additional leverage if the project profitability can justify it — fixing-and-flipping can be a good example of this. Also, always consider smaller projects instead of stretching your budget, as smaller projects can be more economically viable.

Is the repayment obligation sustainable for your budget?

When evaluating the relative burden of your renovation loan, you should take into consideration your existing liabilities and how taking out more loan can impact your daily life. The monthly payment obligation of a renovation loan can range from S$300 to S$1,000 depending on the terms of the loan, representing 3-15% of financial burden on an average Singaporean household’s budget. While this may not seem a lot, financial commitments can snowball into a big portion of your monthly income.

Under the Total Debt Servicing Ratio (TDSR) rule enforced by the Monetary Authority of Singapore, your household liabilities (mortgage, renovation loan, student loan, etc.) cannot exceed 60% of your monthly income. Therefore, if an additional renovation loan pushes you towards this limit, you may want to think twice about borrowing, even if you think your renovation project will ultimately give you good returns.

Parting Thoughts

Homeowners can increase their home’s value by stretching their budgets and utilising home renovation loans. They should be careful, however, about the increasing cost of borrowing as well as the decreasing returns as the project size grows. Finally, they should consider the relative impact of the payment obligation on their monthly budgets, in order to enjoy a better living environment and reap the financial reward of their remodeling projects.

The article 5 Things You Didn’t Know Before Embarking on a Home Renovation Project originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

Source: ValuePen