There have been many reports of the narrowing wage gap in Singapore. For instance, Singapore’s Gini coefficient, the most commonly used indicator of income inequality, has reached 0.458 in 2016, its lowest level in a decade (it was -2.6% lower than its level of 0.470 in 2006). Gini coefficient after account for government transfers and taxes shows an even more dramatic decline in wage inequality, with figures declining from 0.418 in 2006 to 0.402 in 2016. Many people, however, many not feel its effect in their daily lives, and there might be a reason why. As always, the devil is in the detail.

Income Gap Has Actually Widened Since 2000

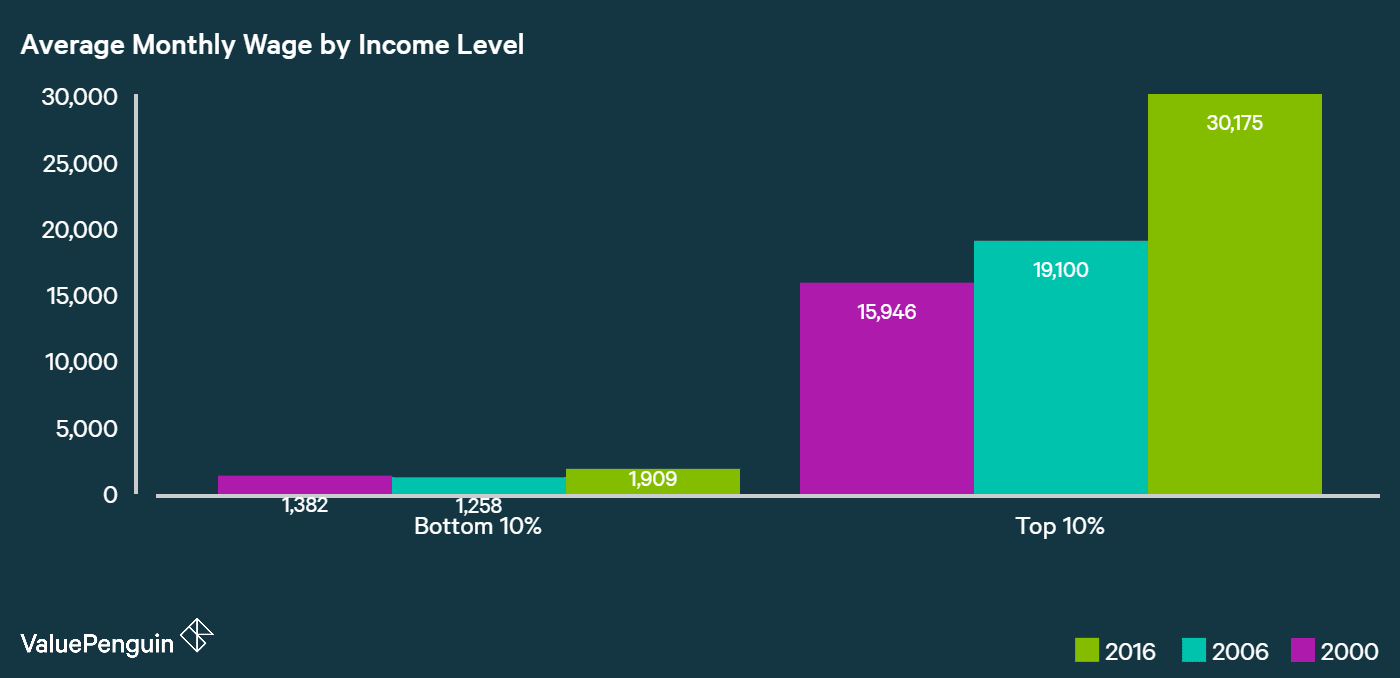

Although Singapore’s wage gap may have declined somewhat since 2006, data shows that it has actually widened quite meaningfully since 2000. For instance, the top 10% of households in Singapore made S$15,946 per month in 2000, roughly 3.02x of S$1,382 of bottom 10% households in the country. By 2016, however, the top 10% made S$30,175 per month, which is 3.19x of S$1,909 that the bottom 10% made. All in all, the top 10%’s income grew by 89% since 2000, while the bottom 10%’s wage grew by only 38%, barely outpacing overall inflation of 32%.

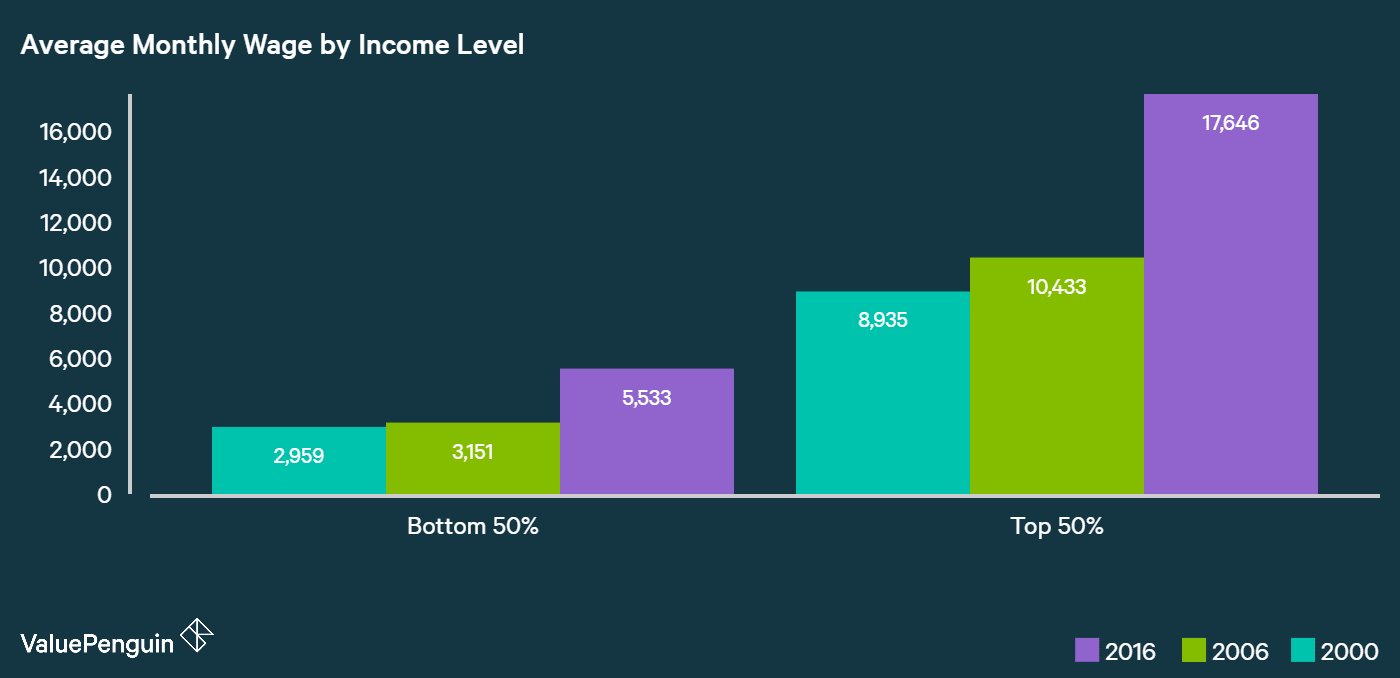

Such a trend wasn’t unique to the top and bottom ends of the spectrum. In fact, there was a similar trend between the top half and the bottom half of the country. The average monthly income of the bottom 50% of households in Singapore, for example, was S$2,959 in 2000, which grew by 87% to S$5,533 in 2016. In contrast, the average monthly income of the top 50% grew by 97% from S$8,935 in 2000 to S$17,646 in 2016. The ratio between the two groups’ wages widened from 11.54 in 2000 to 15.18 in 2006 and 15.81 in 2016.

Low Income Consumers Borrowing to Compensate

In light of these findings, it’s unsurprising that Singapore household’s consumer debt has been rising. ValuePenguin’s study found that personal loans and credit card debt has risen by 188% since 2000, and now makes up 21% of total household debt, compared to just 17% in 2000 to 2006. Given that personal loans and credit card debt are mostly used to fund consumption needs, it seems like the bottom half of the country may have been borrowing to compensate for their lack of relative income growth.

However, it’s important to emphasise the importance of using these financial instruments properly. While it may be tempting to use loans and credit cards to buy things you can’t immediately afford, doing so without the means to repay your obligations on time and quickly can have devastating effects on your life. For instance, the +5% cash back you can earn on credit cards, though extremely generous, compare poorly to 25-28% charges you face on your balance if you fail to pay down all of it within your current billing cycle. That’s not to say that there’s no value in using these products. Properly using some of the best cards could help you save thousands of dollars, while personal loans are meant to help you when you have an immediate and desperate need for cash. Instead of using these instruments to finance your expensive impulses, therefore, it would be wise to spend only what you can afford and borrow only what you can repay quickly and on time.

The article Has the Wage Gap in Singapore Really Been Closing? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Best Debt Consolidation Plans 2017

- Best Personal Loans in Singapore 2017

- Best Rewards Credit Cards 2017

Source: ValuePen