You’ve been working for quite a few years, saving money to buy your home one day. You are getting married, and now you’ve finally saved enough to make it happen. However, with homes easily costing close to a million dollars or more, you won’t be able to do it without the help of some bank financing. But, how much should you really borrow? While it’s rather easy to figure out how much you are allowed to borrow by the government and banks in Singapore, it’s a whole another issue when you are trying to assess how much home loan you should be getting. If you are one of those people, this guide can help you get started in getting to your answer.

How much should you expect to pay for your home?

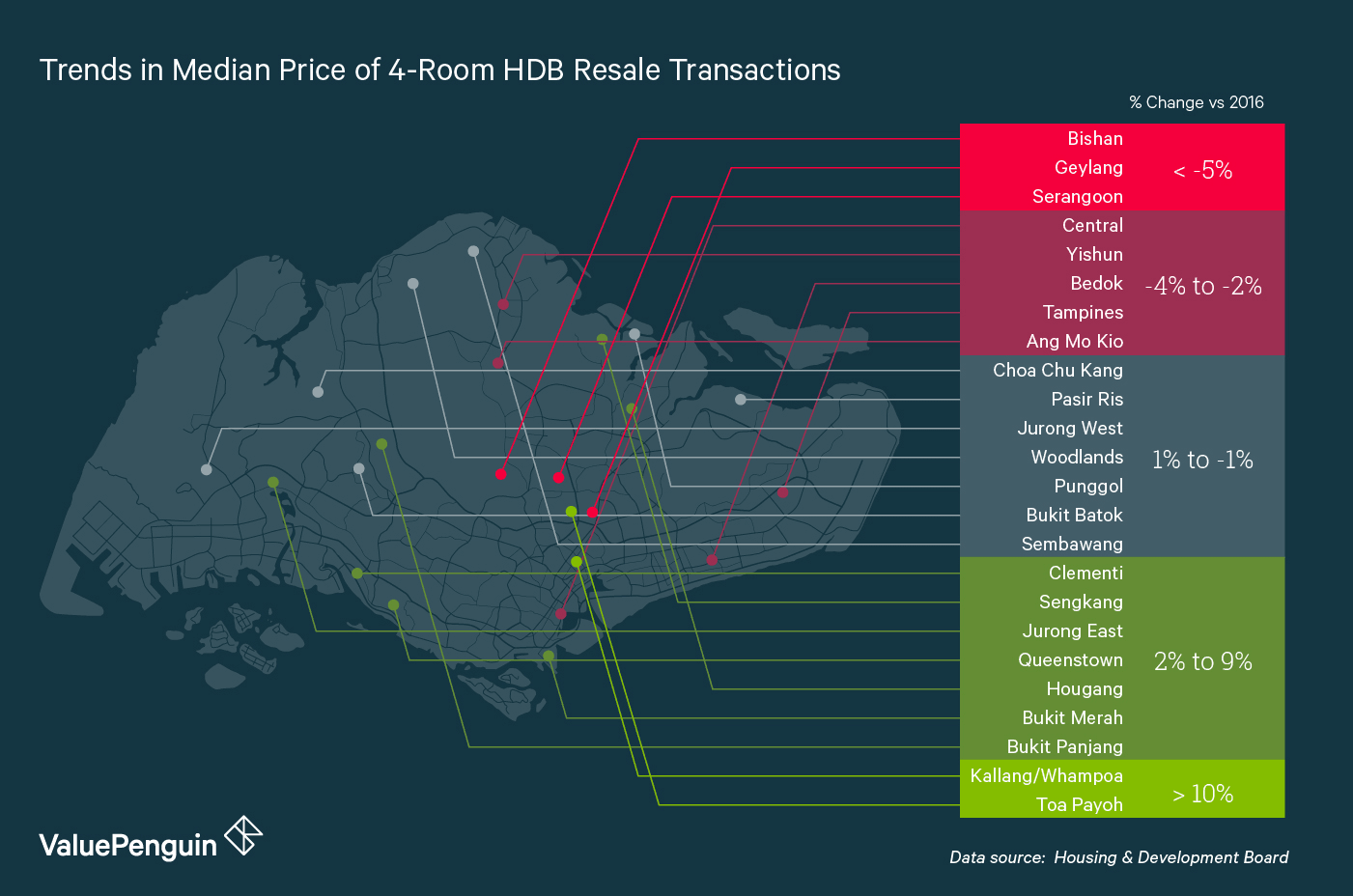

In order to help you understand the approximate cost of a home these days in Singapore, we collected the median price of 4-Room HDB Flat resales by town. According to the data released by the Housing & Development Board, you can expect to pay anywhere between S$350,000 and S$900,000 for a 4-room HDB flat, depending on which town you are residing. Given that most 4-room HDBs are generally around 1,000 sq ft, this translates to around cost of S$350 to S$900 per square foot.

| Town | Q4 2014 | Q4 2015 | Q4 2016 | Q1 2017 | % chg |

|---|---|---|---|---|---|

| Ang Mo Kio | 418,000 | 464,000 | 469,000 | 460,000 | -1.90% |

| Bedok | 497,500 | 415,000 | 419,800 | 410,000 | -2.30% |

| Bishan | 420,000 | 535,000 | 602,000 | 547,500 | -9.10% |

| Bukit Batok | 455,000 | 402,000 | 405,000 | 411,000 | 1.50% |

| Bukit Merah | 425,000 | 640,000 | 604,000 | 630,000 | 4.30% |

| Bukit Panjang | 435,000 | 350,000 | 345,000 | 358,000 | 3.80% |

| Central | 451,000 | 835,000 | 845,000 | 811,500 | -4.00% |

| Choa Chu Kang | 418,000 | 353,000 | 345,000 | 343,000 | -0.60% |

| Clementi | 610,000 | 535,000 | 518,000 | 530,000 | 2.30% |

| Geylang | * | 500,000 | 550,000 | 513,800 | -6.60% |

| Hougang | 391,000 | 398,000 | 380,000 | 390,000 | 2.60% |

| Jurong East | 667,500 | 416,000 | 403,800 | 410,000 | 1.50% |

| Jurong West | 380,000 | 380,000 | 376,900 | 375,000 | -0.50% |

| Kallang/Whampoa | * | 546,000 | 518,000 | 574,000 | 10.80% |

| Pasir Ris | 425,000 | 397,000 | 400,000 | 395,000 | -1.30% |

| Punggol | 515,000 | 420,000 | 450,000 | 452,500 | 0.60% |

| Queenstown | 525,000 | 699,000 | 680,000 | 702,500 | 3.30% |

| Sembawang | 375,000 | 360,000 | 361,500 | 365,000 | 1.00% |

| Sengkang | * | 402,900 | 408,000 | 415,000 | 1.70% |

| Serangoon | 430,000 | 428,000 | 465,000 | 443,800 | -4.60% |

| Tampines | 400,000 | 420,000 | 430,000 | 423,000 | -1.60% |

| Toa Payoh | 368,000 | 530,000 | 565,000 | 631,000 | 11.70% |

| Woodlands | 583,500 | 365,000 | 350,000 | 350,000 | 0.00% |

| Yishun | 357,000 | 354,000 | 369,000 | 356,000 | -3.50% |

Cost of a private residences, on the other hand, was much higher than cost of HDBs, as one would expect. The median transaction price for all private properties ranged from S$800,000 to S$2,700,000, depending on the town, a much bigger variation than that of HDBs. Because the size private residences vary a lot more than HDBs, we also calculated the median price per square foot of all private residence transactions, which ranged from S$750 to S$2,000 depending on the neighborhood.

| Postal District | 2014 | 2015 | 2016 | 2017 YTD | % chg |

|---|---|---|---|---|---|

| 1 | 2,220 | 2,118 | 2,027 | 2,008 | -1% |

| 2 | 2,005 | 1,914 | 1,812 | 1,824 | 1% |

| 3 | 1,666 | 1,625 | 1,639 | 1,682 | 3% |

| 4 | 1,475 | 1,383 | 1,368 | 1,602 | 17% |

| 5 | 1,248 | 1,182 | 1,200 | 1,282 | 7% |

| 8 | 1,956 | 1,300 | 1,205 | 1,448 | 20% |

| 9 | 3,072 | N/A | 3,577 | 1,924 | -46% |

| 10 | 1,331 | 1,484 | 1,520 | 1,858 | 22% |

| 11 | 1,417 | 1,481 | 1,553 | 1,593 | 3% |

| 12 | 899 | 2,056 | 912 | 1,267 | 39% |

| 13 | 1,191 | 1,200 | 1,130 | 1,373 | 22% |

| 14 | 1,131 | 1,055 | 1,087 | 1,557 | 43% |

| 15 | 1,335 | 1,290 | 1,161 | 1,678 | 45% |

| 16 | 1,002 | 968 | 903 | 1,384 | 53% |

| 17 | 846 | 929 | 802 | 834 | 4% |

| 18 | 790 | 960 | 780 | 1,015 | 30% |

| 19 | 1,174 | 1,116 | 1,039 | 1,046 | 1% |

| 20 | 1,194 | 1,239 | 1,099 | 1,258 | 14% |

| 21 | 1,297 | 1,263 | 1,178 | 1,140 | -3% |

| 22 | 897 | 858 | 723 | 821 | 14% |

| 23 | 1,031 | 916 | 904 | 791 | -13% |

| 25 | 867 | 788 | 708 | 761 | 7% |

| 26 | 1,136 | 1,085 | 1,046 | 1,040 | -1% |

| 27 | 874 | 757 | 489 | 812 | 66% |

| 28 | 1,150 | 1,133 | 901 | 870 | -3% |

Latest Real Estate Price Trends: Property Prices Are Generally Falling in Singapore, But Mostly in Central

What was also interesting was that property prices have been falling in central, but not everywhere in Singapore. According to ValuePenguin’s study, the median price of 4-room HDBs (the most common type of housing in Singapore) has fallen by -4% in Central so far in 2017 compared to its level in Q4 of 2016. In contrast, the resale price of 4-Room HDBs in areas like Toa Payoh and Bukit Merah actually increased.

This trend of property price was even clearer for private residences. Data from Urban Redevelopment Authority shows that the median private property price per square foot in central declined by -46% to S$1,924 so far in 2017 from S$3,577 in 2016. However, there were meaningful increases in private property prices in non-central districts, as shown in our map below. While the overall market was in an overall decline on average, the most of the decline was concentrated in the central area (i.e. postal district #9).

Don’t Maximise Your TDSR or LTV Limit

Given these high prices, it’s almost a necessity get some bank home loans when you are purchasing your first home. For instance, Singaporeans have been borrowing about 53% of their home value to fund their purchases in Q1 of 2017. What’s concerning is that this average loan-to-value (LTV) ratio in Singapore has risen from 48% in 2014.

We think borrowing an increasing amount to fund your home purchase might not be the best idea, especially in face of a declining real estate market. It is good to borrow while interest rates are still at historically low levels, but rising SIBOR coupled with declining property prices can really hurt you when your home loan’s fixed rate resets to floating rates in a few years time. Given this, make sure you don’t borrow too much more than 50% of your home value, so that you can still manage to pay your interest when rates are higher in 3 years.

The article originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

- Average Household Debt in Singapore 2017

- Best Personal Loans in Singapore 2017

- Best Renovation Loans 2017

Source: ValuePen