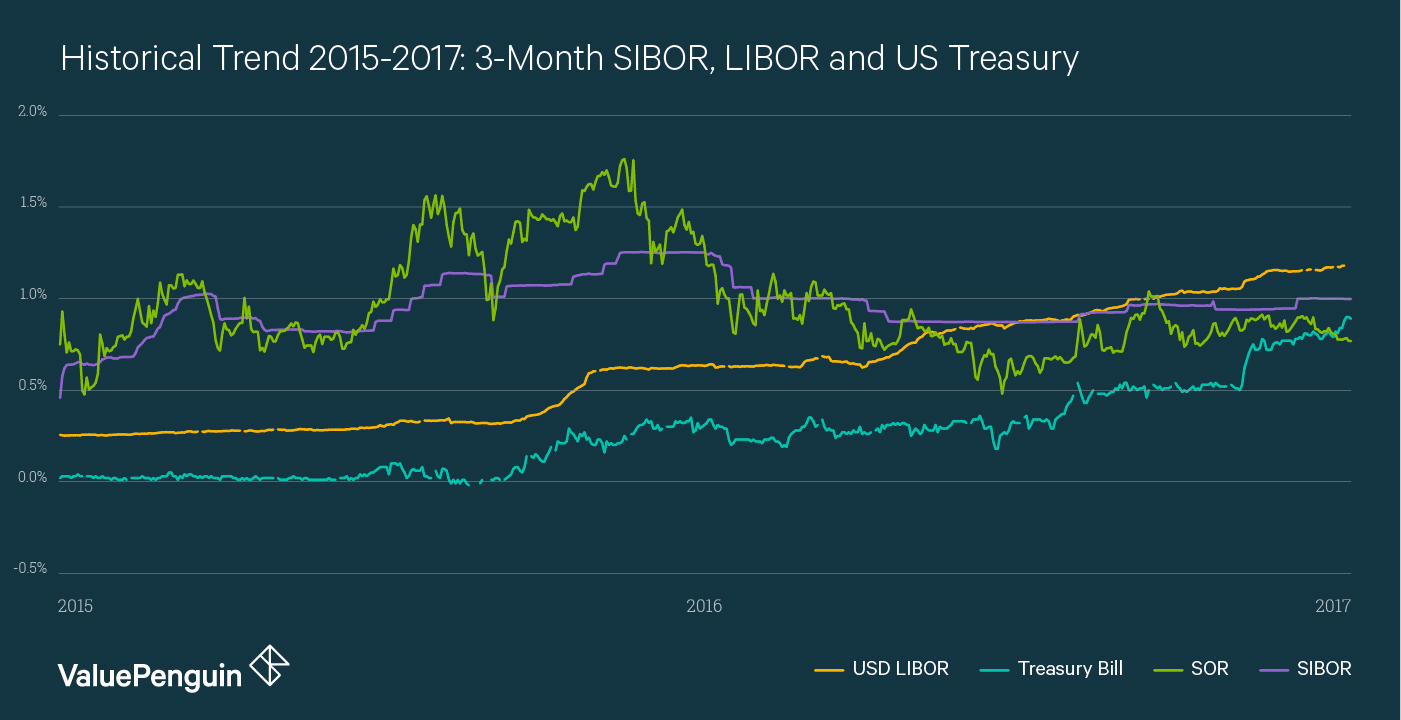

After floating around 0.4% for +5 years, 3-Months SIBOR has risen to around 1% by May of 2017. This is because the U.S. central bank began to hike its interest rates since 2015. However, although rates in the US have continued to increase ever since, 3-Month SIBOR has actually fallen recently from 1.2% in March 2016. This could be a rather confusing phenomenon for an average consumer, especially if he is trying to decide if he should be refinancing his home loan before rates to up even more. Will SIBOR continue to be decoupled from the US rate, and even go down more from here? Or will it eventually catch up with the US rates and continue its rise? Here, we breakdown a few facts to help you make a better financial decision.

US Rates & SIBOR Have Long-Term Correlation

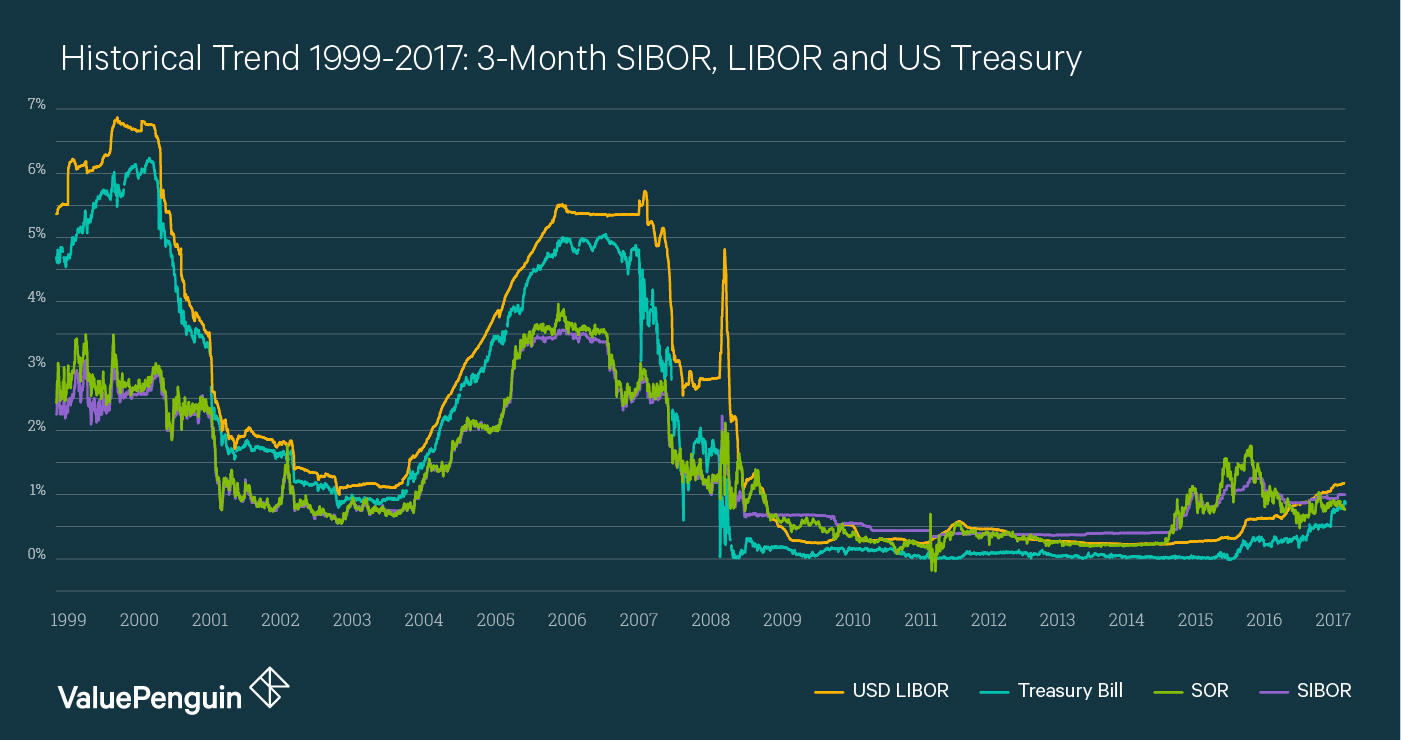

Although you can see from the charts above that SIBOR and US rates have not moved in tandem since 2015, there’s an undeniable correlation between the two rates, especially in the long run. This is because the Monetary Authority of Singapore, Singapore’s central bank, regulates its interest rates primarily in order to control Singapore Dollar’s exchange rates. When US Rates go up, the value of US Dollar goes up, making SGD and/or other currencies relatively less valuable. Therefore, MAS has to eventually increase rates to keep SGD’s exchange rates steady over the long run, especially if other are doing the same. Therefore, as you can see in the chart below, SIBOR and US rates have largely moved together since 1999.

This disconnect in short term relationship and long-term relationship between the rates is extremely apparent in correlation data. For example, the correlation between 3-Month SIBOr and 3-Month US Treasury rates was 92.9% from 1999 to 2017. However, within this time period, the annual correlation between the two rates were above 90% only in 2004, and has been as low as -36% in 2010.

| Correlation Between | 3-Months SIBOR & LIBOR | 3-Months SIBOR & US Treasury |

|---|---|---|

| 1999-2017 | 92.9% | 92.9% |

| 1999-2008 | 88.0% | 88.1% |

| 2009-2017 | 46.5% | 56.4% |

| 1999 | 64.5% | 78.2% |

| 2000 | 65.5% | 40.2% |

| 2001 | 79.1% | 79.6% |

| 2002 | 25.2% | 21.9% |

| 2003 | 8.5% | 3.3% |

| 2004 | 92.6% | 92.4% |

| 2005 | 85.6% | 82.7% |

| 2006 | 75.2% | 76.1% |

| 2007 | 31.2% | 48.8% |

| 2008 | 80.1% | 57.5% |

| 2009 | 34.7% | -9.2% |

| 2010 | -17.7% | -35.7% |

| 2011 | -58.4% | 60.4% |

| 2012 | 71.9% | -41.3% |

| 2013 | -71.3% | 14.0% |

| 2014 | 63.2% | -24.0% |

| 2015 | 65.0% | 45.2% |

| 2016 | -69.4% | -26.1% |

| 2017 | -67.9% | -21.1% |

Astute observers may have noticed that correlation between SIBOR and US rates have gone down dramatically since 2008. This is because US rate policies have not been uniformly followed by all other central banks in the world. Since Singapore has many trading partners in Asia, it has to balance its exchange rate against many other currencies outside of USD. Therefore, MAS had to keep SIBOR relatively steady in 2016 even as US kept raising its rates because other countries like China and Japan were lowering their own interest rates.

It’s rather difficult to predict exactly how SIBOR will behave over the next 12 to 24 months. If anyone is very accurate with this type of predictions consistently, they would probably one of the the richest people in the world. It’s certainly possible that the whole world outside of the US continues to lower rates, and therefore SIBOR continues to deviate from US rates. If history is a good indicator, however, SIBOR should eventually move with the US rates over the long-run spanning multiple years, partly due to the US Dollar’s economic importance in the world.

So Should You Refinance Your Home Loan Before Rates Go Back Up?

The answer to this question is, always: it depends on when you got your loan. Typically, all home loans in Singapore are priced as floating rates after the first 3 years of their tenures, if not shorter. This means that no matter if you got your home 3 years ago or 10 years ago, you are probably paying whatever the market rate is right now, and will pay higher or lower rates as SIBOR moves up and down every month. For people who got their loans 3 years or more years ago, it might be a good idea to refinance their home loans now to lock in what is still relatively low rates in a historical perspective (with the caveat that you have to believe rates will continue to go up over the next few years).

Also, if you got your home loan sometime between September 2015 and June 2016, it might be a good idea to refinance now since rates have come down meaningfully since then (with the caveat that your loan’s terms allow you to do so without a big penalty). Whatever you do, you should make sure to research more about SIBOR and the foreign exchange market to try and form your own opinion about where SIBOR is going. Also, make sure to compare the best home loans online so you can take full advantage of refinancing to save on your interest payment.

The article Rising SIBOR: Should You Refinance Their Home Loans Now? originally appeared on ValuePenguin.

ValuePenguin helps you find the most relevant information to optimise your personal finances. Like us on our Facebook page to keep up to date with our latest news and articles.

More From ValuePenguin:

Source: ValuePen